Last Updated on November 11, 2025 by Luxe

Key Takeaways

- Debt consolidation simplifies multiple debts into one manageable monthly payment.

- Options and other lenders allow borrowers to apply online for quick access.

- Consolidation can lower interest rates and improve credit, but risks include fees, longer terms, or new debt accumulation.

- Alternatives such as debt management plans, direct negotiations, or DIY repayment strategies may also be effective.

- Success depends on discipline, comparing lenders, and avoiding new debt after consolidating.

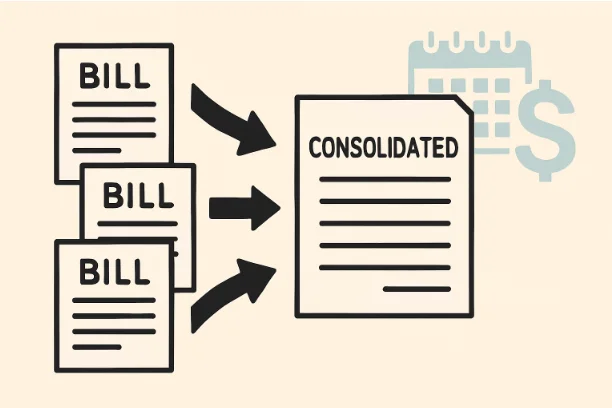

What Is Debt Consolidation?

Debt consolidation combines several debts, often high-interest credit card balances, personal loans, or other unsecured debts, into a single loan with one monthly payment. Many people pursue debt consolidation to simplify their finances, potentially lower interest costs, and make repayment more manageable. The debts you can typically consolidate include credit cards, medical bills, store cards, payday loans, and sometimes personal loans.

There are various ways to get a consolidation loan, from local banks and credit unions to specialized online lenders such as MaxLend loans. Depending on your credit and financial situation, these options can offer different rates, approval requirements, and terms.

How Do Debt Consolidation Loans Work?

Consolidating debt starts with applying for a new loan large enough to pay off your debts. After approval, you’ll use the funds to pay off those balances, leaving just one monthly loan to manage. For example, if you have three credit cards and a personal loan, you could use a debt consolidation loan to pay them all off, resulting in a single monthly payment, potentially at a fixed rate. In many cases, borrowers can apply online, MaxLend loan to explore consolidation options quickly and conveniently.

Debt consolidation loans usually come in two forms: those with fixed interest rates, which offer predictable payments, and those with variable rates, which can fluctuate over time. Fixed rates are often preferable for borrowers who want consistency and to avoid surprises on their monthly bills.

Potential Benefits of Consolidating Debt

- Simplified Repayment: Managing one monthly bill instead of several can reduce stress and minimize the chances of missing a payment.

- Lower Interest Rates: Consolidation loans, especially with good to excellent credit, may offer significantly lower rates than your existing debts, helping you pay less over time.

- Improved Credit Over Time: Consistent on-time payments and decreased credit card balances can improve your credit utilization ratio and positively affect your credit score.

What Are the Risks and Drawbacks?

- Fees and Higher Rates: Some borrowers, particularly those with lower credit scores, may only qualify for loans with high fees or interest rates that don’t offer real savings.

- Temptation to Take on More Debt: After consolidating, it is crucial to avoid accruing new debt on paid-off credit cards, which can worsen your financial situation.

- Longer Repayment Timelines: By spreading payments over a longer period to achieve lower monthly payments, you might pay more in total interest, even if the rate is lower.

Is Debt Consolidation Right for You?

Assess your full financial picture before proceeding. Do you have a steady income to support monthly payments? Is your credit strong enough to secure favorable loan terms? Are you willing to change financial habits to avoid new debt?

- Review the total interest cost, not just the monthly payment.

- Factor in any loan origination fees or penalties.

- Ask yourself whether you need professional help. Sometimes, working with a credit counselor or even considering bankruptcy may be better than consolidation.

Alternatives to Debt Consolidation

If debt consolidation isn’t a good fit, explore these alternatives:

- Debt Management Plans (DMPs): Nonprofit credit counseling agencies can help you work with creditors to set up a repayment plan, often with lower interest rates and fees.

- Negotiating Directly With Creditors: In some situations, lenders may agree to lower your interest rate or accept a lump-sum payment for less than the full debt amount.

- DIY Repayment Strategies: The debt snowball (paying off smallest balances first) and debt avalanche (paying off highest interest debts first) methods offer structured ways to tackle multiple debts without taking out a new loan. For tips on choosing a repayment strategy.

How to Find a Reputable Lender

- Research Credentials: Look for reviews, check for state licensing, and confirm a lender’s standing with the Better Business Bureau.

- Read the Fine Print: Always review the full terms, including the APR, fees, and penalty clauses, before signing away from the deal.

- Trusted Resources: For more information and tips on choosing a consolidation loan.

Real-Life Outcomes: What Research Says

Recent studies reveal that debt consolidation can improve borrower outcomes if the new loan has a significantly lower interest rate and the consumer avoids accruing new debt. According to a Forbes Advisor report, consolidation works best with a clear budget and strong financial discipline. Financial advisors recommend comparing multiple lenders and loan offers before deciding, as terms and interest rates vary widely.

Industry data has shown that roughly 60% of individuals who consolidate their debt see an improvement in their credit score within one year, provided they make on-time payments and refrain from taking on new unsecured debt.

Wrapping Up: Making an Informed Choice

Debt consolidation loans can be helpful for borrowers looking to simplify repayment and reduce the cost of their debt, but only when approached with a full understanding of both benefits and risks. Always compare options, read the loan terms carefully, and seek professional advice if you’re unsure. Debt consolidation can be an effective step toward financial wellness and peace of mind when used wisely and as part of a broader plan to build healthy financial habits.